We collaborate with clients as they strive to solve customer loyalty challenges, and customers being customers, these challenges are complex, subtle, and fluid. And they occur in the context of an industry which is being disrupted.

The rate of change is particularly high at the moment, a pause and review could help as we try to understand the consequences of the perfect storm; GDPR, cookies going, apple permission-based tracking, EU Civil Liberties actions, skepticism about the effectiveness of programmatic marketing… What does all of this mean for customer loyalty? Why are retailers transforming like werewolves on a full moon?

Our attempt at explaining what has / is going on may be helpful, or at least interesting? We would love to talk with you about it.

There is a two-sided market for selling stuff

The business of selling to consumers is simple in principle but complex in fact. On one side is a population of buyers looking for a good deal, on the other a collection of merchants looking for buyers. Two-sided markets cry out for market operators to connect the two groups, buyers, and merchants, and vice versa.

Like most ‘dances for three,’ the arrangement gets complicated, quickly. Especially as we introduce technology.

Merchants looking for buyers

Let’s start with a look at the Merchant side of the market. This has been guided by the ‘cost per impression’ models of mass advertising and ‘The Attention Economy’1, with its belief that the critical resource is customer attention. ‘Look at me!’ marketing resulted with operators aggregating deals and discounts/remarkable offers in an attempt to attract attention. The internet made this easier, so affiliate shopping malls, cashback shopping programs and Amazon grew dramatically.

In many ways this ‘fresh’ marketing channel emulated the mass advertising channels it supplemented; intrusive, undifferentiated, blurrr.

Just as merchants worried about the 50% of their advertising, they were wasting2, now they worried about the discounts they were giving to customers who already intended to buy at full price. And as media channels proliferated, the selection of the best became a daunting task.

The need to increase marketing conversion rates incubated ‘The Intention Economy’ thinking: “The intention economy is an approach to viewing markets and economies focusing on buyers as a scarce commodity. Customers’ intention to buy drives the production of goods to meet their specific needs.3 ” We hope customers with an intention to buy are easier to sell to.

The challenge is in detecting this intention early enough to influence their decision on what exactly they buy to get their job done, and from whom to buy.

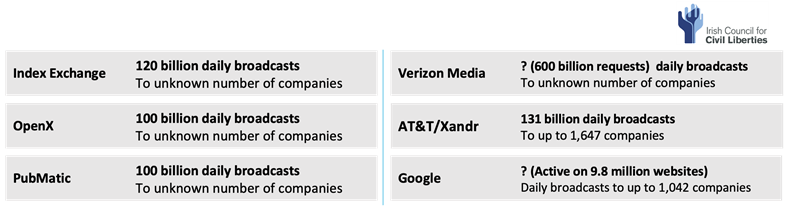

The surveillance marketing platforms stepped in to build ‘prediction markets’ selling ‘intentions’ inferred through user browsing history and site characteristics. Google, Facebook, and other web publishers participating in Real Time Bidding platforms are now powerhouses. To advertisers the claim is that digital offers will be presented to consumers who have an intention (or at least an interest) in what you have to say. The volumes involved are impressive4;

The biggest data breach ever recorded

Tracking-based ads (RTB) broadcasts by biggest “ad exchanges”

Since customer intent is inferred, not measured, it is difficult to ensure sales can be attributed to the investment in programmatic ad placements. Lack of accountability has resulted in some ‘slack’ in the system apparently, “…Half of Google’s ad revenue once came from helping publishers show ads on publisher’s own properties. But now nearly all (85%) of Google’s ad revenue comes from displaying ads on its own websites and apps, with the benefit of data siphoned from publishers’ websites & apps.”5 And it appears that 35% – 70% of advertising fees paid by advertisers in the tracking-based ad industry go to intermediaries in the process.6

What we see implemented is a far cry from what was described in 2006. In those heady days Marketers thought the customers would be active participants in the selling of Intention, rather than unsuspecting targets.

A robust market of Vendor Relationship Management (VRM) platforms is still to blossom – there are some promising shoots – but the proposition is attractive to consumers and consumer advocates;

‘Free customers are more valuable than captive ones’, and ‘Free markets require free customers.’

“In The Intention Economy, a car rental customer should be able to say to the car rental market, “I’ll be skiing in Park City from March 20–25. I want to rent a 4-wheel drive SUV. I belong to Avis Wizard, Budget FastBreak and Hertz One Club. I don’t want to pay up front for gas or get any insurance. What can any of you companies do for me?”—and have the sellers compete for the buyer’s business.”

Searls, Doc. The Intention Economy. Harvard Business Review Press. 2006

Program Operators looking for Merchant money

Enterprising platform operators compete for the money merchants are willing to invest in attracting customers. By offering,

- Customers a large collection of good deals, low prices and offering

- Merchants large numbers of customers intending to spend, these platforms profit by taking fees for match-making the two.

The fees merchants are willing to pay for customer introductions are used as incentives to attract the customers in the first place. Cash back shopping programs (e.g., Rakuten, CashRewards, Cheddar, ShopBack, Upstreet who convert the cash back to partial shares in the merchant), offer this ‘sweetener.’

To the merchant, these platforms only cost money if sales are made, so little reason not to sign up with all of them, and many do. After all the value proposition is impressions, so the more programs the better. This makes the sales offers like ‘above the line’ offers again, same for everyone and same on every platform, blurrr.

Some of these marketplaces are personalising customer offers based on purchase behaviour, they can do this because they have data on sales actually made to customers, e.g., Amazon and more recently, Little Birdie.

An interesting variant has been presented by the ‘Buy Now Pay Later’ providers, who have partially justified their merchant fees by helping the merchant market to their growing customer databases7. Klarna’s acquisition of the ‘shopper’s friend’ Hero strives to make this BNPL vendor a shopping, rather than payment, destination for their customers.

There has also been a realisation that first party data allows more effective marketing leads and the next disruption… the full moon.

Already have an audience, and already have permission? Become the targeting operator! Make other merchants pay.

Organisations with large databases of ‘first party’ data (data from the customers directly as they did business) have for many years understood the value this data has in guiding their interactions with customers. These data assets are from loyalty programs, contractual relationships, including subscriptions or even the delivery records of shoppers buying online.

Using this data can improve relationships (and sales) with your customers but recently it has also occurred to the data-owners that they could use this asset to help other merchants sell to these same customers, for a fee. In most cases they can measure customer intention not just infer it, correctly attribute sales to promotions, and do all of this with the permission and active collaboration of the customer.

Transaction-informed marketers have well-developed data muscles and can develop prediction markets of their own, in some cases they can just ask the customer. Lycanthropy makes this pool of customer intention available to other merchants / advertisers, in competition to the surveillance folks like Alphabet and Meta.

There are plenty of examples;

- The US grocery giant Kroger with a cloud platform based on its loyalty program8. Tesco in the UK have a similar offering9.

- Amazon with a ‘Data Clean Room’10 for merchants

- In Australia, the two large grocers have media companies fueled with loyalty program data; Coles have ‘Unpacked’11 , Woolworths have Cartology12.

It is not just retailers entering this market for customer intention; Australia’s largest bank, CBA, is investing heavily on a number of fronts to build customer intention assets. They have invested in Klarna (who has added Hero to help its customers & merchants13), added Little Birdie and Cheddar to their banking app14, both ‘deal seeking’ platforms and the big one, a large investment in the Artificial Intelligence platform H2O.ai15 to help predict purchase intention using the rich data a bank has on its customer’s shopping behaviour.

CBA has even become the solution for customer intention by acquiring electricity and telecommunications companies – most customers do intend to turn on the lights and make a phone call.

There is at least one vendor16 who offers to apply AI to client-bank’s data, identifying pockets of customer intention to buy or switch, then offers this demand to potential suppliers in an auction marketplace (similar to RTB). Being banks, they can then present the offers and report on actual sales for the winning bidder.

Are payment schemes entering the contest?

The payments schemes, Visa, MasterCard, Amex, Discover, JTB, CUP etc. all have very large data assets and have dabbled in providing data services to merchants17. Mastercard promote access to data from 2.4 billion cards and 65 billion transactions for year, and they are smaller than Visa!

But their data is anonymised, they do not know individuals, just cards and they do not see what the customer purchased, just how much they spent. Enter Consumer Data Right regulation and Open Banking. Mastercard has announced they will be certified as a data recipient (in Australia) and will act as a ‘middleware’ enabler to service providers who can leverage payment and banking data to offer richer consumer and merchant services. And most importantly, give consumers reasons to provide permission to use the data.

Mastercard has acquired two companies already established in the ‘CDR’ data market; Finicity and aiia, Visa has acquired Tink for the same purpose. Stay tuned, the rate of change in payments data will only accelerate.

Where is the silver bullet? Who you going to call if you do not have a large first party data asset, to compete? Or do not have the data muscles?

The ‘rise’ of First Party Data markets is good news for the large retailers, large banks, global payment schemes… but how do you compete if you are not in this category of corporations?

You can pay to use their data of course, using them as marketplace operators, for a fee while enhancing their data for resale to (potentially) your competitors.

The alternative is to participate in collaborative commerce with like-minded organisations and assemble a data asset of equivalent value to a network of companies with first party data they would like to enhance and employ for marketing, with permission, while preserving customer privacy. Privacy-Enhancing Technologies are available that allow organisations to do exactly this…

References:

- The Attention Economy John C. Beck and Thomas H. Davenport 2001

- Ironically, not much has changed really; “Last year, a study by the UK’s ISBA (Incorporated Society of British Advertisers) found that half of every advertising dollar spent on tracking-based programmatic advertising disappears in the adtech ecosystem before it reaches a publisher.” The Ad Contrarian, Nov 21, 2021

- Doc Searles 2006, Linux Journal

- Sustainability without surveillance – Irish Council for Civil Liberties (iccl.ie)

- Sustainability without surveillance – Irish Council for Civil Liberties (iccl.ie)

- Ibid. There is a growing number of case studies where companies have discontinued multi-million dollar investments in programmatic marketing, particularly paid search, with zero impact on sales revenue; eBay & Uber being the best American examples.

- “We’re looking to deliver much more insightful information than just customer segmentation. The IQ platform can provide a deeper understanding of the customer, ideas for new channels to target that customer and even new product ranges or adjacencies.” Afterpay Afterpay IQ gives retailers keys to BNPL world of instant shopping gratification (theaustralian.com.au)

- Kroger unveils collaborative cloud platform

- Tesco Media & Insight Platform – dunnhumby

- Amazon’s Data Clean Room

- Unpacked by Flybuys

- Cartology | We get customers

- Klarna acquires HERO to bring best of in-store experience to social shopping for its 90m consumers

- CBA adds ‘Spotify of shopping’ to its ‘super app’ play CBA launches Cheddar: New ‘Tik Tok of shopping’ app arrives ahead of Black Friday sales | news.com.au — Australia’s leading news site

- H2O.ai | AI Cloud Platform

- Krowd (krowdit.com)

- Data & Analytics | Mastercard Data & Services (mastercardservices.com)